Have you ever watched a snowball roll down a hill? It starts small. But as it rolls, it picks up more snow. It gets bigger and bigger. By the time it reaches the bottom, it is huge.

Money can do the same thing. And the secret is called compound interest.

Let’s learn what it is, how it works, and why it matters even for kids.

What Is Interest?

First, let’s talk about plain interest. This is what a bank pays you for keeping your money there.

Think of it like rent. You let the bank use your money. The bank pays you a little extra for that. That little extra is called interest.

For example, say you put $100 in a savings account. The bank pays you 5% interest per year. After one year, you get $5. Now you have $105.

Simple, right? But here is where it gets really exciting.

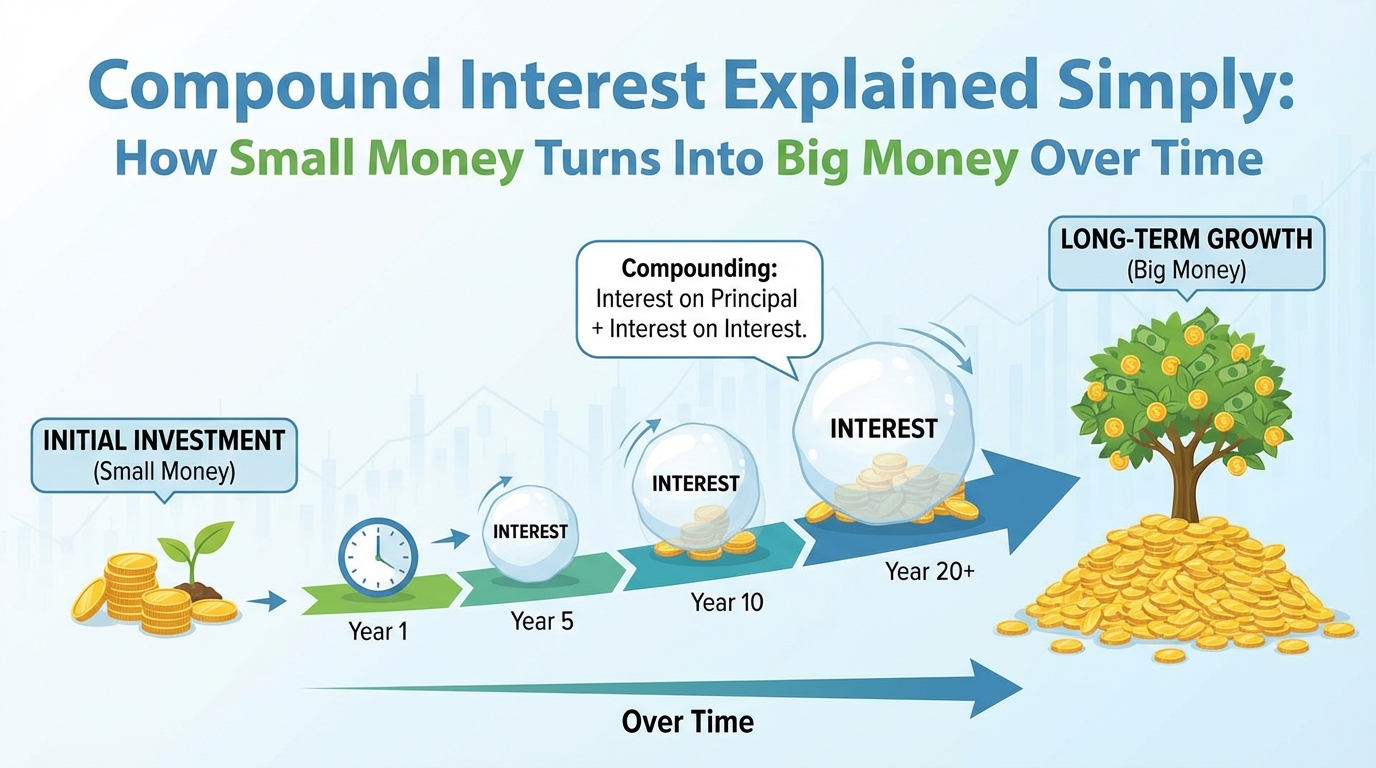

What Makes Compound Interest Special?

With compound interest, the bank does not just pay you interest on your original money. It also pays you interest on the interest you already earned.

Let’s go back to that $100 example.

- Year 1: You earn $5. Now you have $105.

- Year 2: You earn 5% on $105 not just $100. That is $5.25. Now you have $110.25.

- Year 3: You earn 5% on $110.25. That is $5.51. Now you have $115.76.

Each year, you earn a tiny bit more than the year before. Your money is growing on top of itself. That is the power of compounding.

A Simple Way to Picture It

Imagine you have a magic tree. Every year, the tree grows new branches. And every new branch grows its own branches the next year.

At first, the tree does not look much different. But after 10, 20, or 30 years? That tree is enormous. You cannot even count all the branches.

Compound interest works just like that magic tree. The longer you let it grow, the bigger it gets.

Real Numbers: Watch $1,000 Grow

Here is a real example using 7% yearly interest close to what a long-term stock index fund has earned on average historically, according to data from the U.S. Securities and Exchange Commission (SEC).

| Years | Money Grows To |

| 10 years | ~$1,967 |

| 20 years | ~$3,870 |

| 30 years | ~$7,612 |

| 40 years | ~$14,974 |

You put in $1,000 and never added more. After 40 years, you have nearly $15,000. Your money grew almost 15 times without you doing any extra work.

Note: These numbers are estimates using the compound interest formula A = P(1 + r)^t, where P = $1,000, r = 0.07, and t = years. Real returns vary and are not guaranteed.

The Rule of 72: A Fun Trick

Want to know how fast your money will double? Use the Rule of 72. Just divide 72 by your interest rate.

- At 6% interest: 72 ÷ 6 = 12 years to double

- At 8% interest: 72 ÷ 8 = 9 years to double

- At 12% interest: 72 ÷ 12 = 6 years to double

The higher the interest rate, the faster your money doubles. This is a real math shortcut used by financial experts.

Why Starting Early Is So Important

Here is the big lesson: time is your best friend.

The earlier you start saving, the more time compound interest has to work. Even small amounts matter a lot when you start young.

Let’s look at two kids Maya and Alex.

Maya starts saving $50 a month at age 15. She earns 7% per year.

Alex waits and starts saving $50 a month at age 25. He also earns 7% per year.

By the time they are both 65:

- Maya has saved for 50 years → about $262,000

- Alex has saved for 40 years → about $131,000

Maya did not save more money each month. She just started 10 years earlier. That one choice nearly doubled her total.

Calculations based on the future value of monthly contributions formula. Results are rounded and for illustration only.

Where Does Compound Interest Happen?

Compound interest is not just one thing. You will find it in many places:

It helps you when you save or invest:

- Savings accounts at banks

- Certificates of deposit (CDs)

- Retirement accounts like a 401(k) or IRA

- Index funds and investment accounts

It works against you when you borrow:

- Credit cards (these often charge very high interest 20% or more)

- Personal loans

- Student loans

This is why it is so important to pay off debt fast. The same power that grows your savings can grow your debt, too.

Compound Interest vs. Simple Interest

Here is a quick side-by-side:

| Simple Interest | Compound Interest | |

| What grows? | Only your original money | Your money + your past interest |

| How fast does it grow? | Steady, straight line | Faster and faster over time |

| Best for savers? | Less powerful | Much more powerful |

How Often Does It Compound?

Not all accounts compound at the same speed. Some compound:

- Daily (most common in savings accounts)

- Monthly

- Quarterly (every 3 months)

- Annually (once a year)

The more often it compounds, the slightly faster your money grows. Daily compounding is the best for savers.

3 Easy Steps to Use Compound Interest

You do not need to be rich to start. Here is how anyone can begin:

Step 1: Open a savings account. Even $10 or $20 is a start. Many banks and credit unions have accounts with no minimum balance.

Step 2: Add money regularly. Even a small amount added each week or month makes a big difference over time.

Step 3: Leave it alone. The longer your money sits and grows, the bigger the snowball gets. Try not to take it out early.

Quick Review: What You Learned

- Interest is money the bank pays you for saving.

- Compound interest means you earn interest on your interest, too.

- The longer you save, the faster your money grows.

- Starting early even with small amounts makes a huge difference.

- Compound interest can hurt you if you carry high-interest debt.

The Bottom Line

Compound interest is one of the most powerful money tools in the world. You do not need a lot of money to use it. You just need time and patience.

Albert Einstein is often credited with calling compound interest “the eighth wonder of the world.” While historians debate whether he actually said it, the math behind the idea is very real and very powerful.

Start small. Start now. Let time do the heavy lifting.

Your future self will thank you.

Disclaimer: This article is for educational purposes only. It is not financial advice. For personal money decisions, please speak with a licensed financial advisor. Interest rate examples are for illustration and do not represent guaranteed returns.

Post Disclaimer

The information provided on Financepdia.com is for educational and informational purposes only and should not be considered financial, investment, or trading advice. Cryptocurrency and financial markets are highly volatile and involve significant risk. Readers should conduct their own research (DYOR) and consult with a qualified financial advisor before making any investment decisions. Financepdia.com and its authors are not responsible for any financial losses resulting from actions taken based on the information provided on this website.