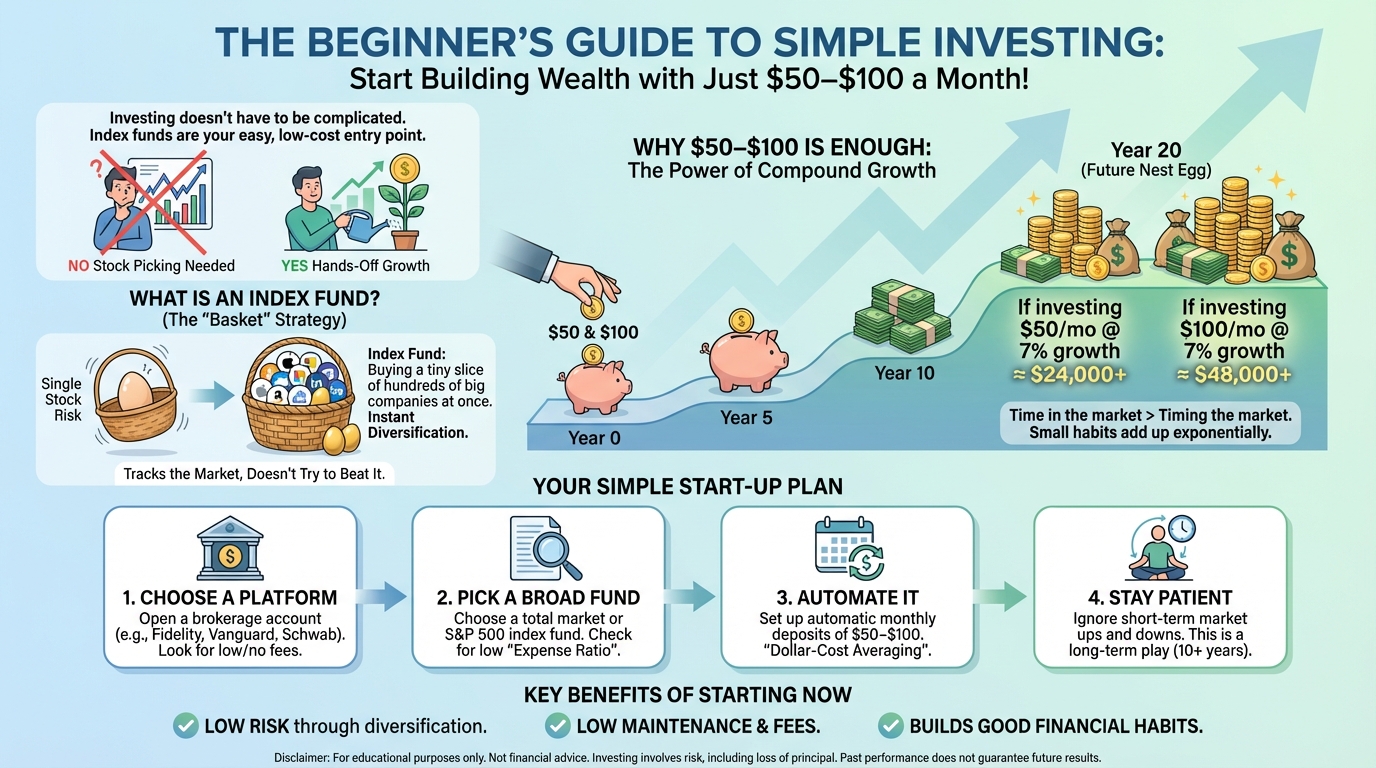

Investing might sound complicated, but it doesn’t have to be. Even if you only have $50–100 per month, you can start building your wealth by investing in index funds. Here’s a simple guide to help you get started.

What Is an Index Fund?

An index fund is a type of investment that tries to copy a big group of stocks called an index.

- Example: The S&P 500 is an index of 500 big U.S. companies like Apple and Microsoft.

- When you invest in an index fund, your money buys a tiny piece of all these companies at once.

- This is safer than buying one single stock because your money is spread out.

Why Index Funds Are Great for Beginners

Index funds are low-maintenance. You don’t need to pick individual stocks or watch the market every day. They spread your risk across hundreds or thousands of companies and have lower fees than actively managed funds. This makes them a simple, safe way to start investing even with small amounts like $50–100 per month.

Types of Index Funds

Index funds come in different flavors, and knowing your options helps you pick the right one:

- ETF index funds: Trade like stocks during the day; good if you want flexibility. Best for occasional investors who like market control.

- Mutual index funds: Trade once daily; perfect for automatic monthly investing. Ideal for small, consistent monthly contributions.

- Sector index funds: Focus on a specific industry, like technology or AI. Use cautiously until you’re more experienced.

- International index funds: Invest in companies outside the U.S. Adds global diversification to your portfolio.

- Bond index funds: Provide stability and income for a balanced portfolio. Good for reducing risk as you age.

- Specialized funds: Trend-focused options like AI or cybersecurity stocks, useful once your portfolio grows. Not recommended for beginners starting small.

Why Index Funds Track the Market

Index funds are designed to match the market, not beat it. This keeps fees low and avoids the risk of picking individual stocks. The goal is long-term growth, making them perfect for beginners who want steady, hands-off investing.

Why $50 -100 Per Month Is Enough

You don’t need thousands of dollars to start. Even small amounts work because of compound growth:

- Your money can grow over time.

- If you invest $50 per month, it adds up every year.

- Over 10–20 years, your small monthly investments can become a big nest egg.

Example:

- $50 per month = $600 per year.

- $100 per month = $1,200 per year.

- Over 20 years, with 7% annual growth, $50/month could grow to about $24,000, and $100/month could grow to about $48,000.

Choose a Platform to Start Investing

You need a platform to buy index funds. These are called brokerages. Some beginner-friendly options include:

- Vanguard: famous for low-cost index funds

- Fidelity: beginner-friendly with no minimums

- Charles Schwab: good for small monthly investments

Tips for Beginners:

- Pick a platform that allows automatic monthly deposits.

- Check for low fees: even small fees can reduce your growth over time.

Pick Your Index Fund

For beginners, some popular options are:

- Vanguard 500 Index Fund (VFIAX): tracks the S&P 500

- Fidelity ZERO Total Market Index (FZROX): no minimum, no fees

- Schwab Total Stock Market Index (SWTSX): broad U.S. market coverage

Step-by-Step:

- Look at the fund’s expense ratio: smaller is better (0.0%–0.1% is excellent).

- Check the fund’s track record: how it grew over the last 10–20 years.

- Decide how much to invest monthly.

Set Up Automatic Investments

Automatic monthly deposits make investing easier and more consistent:

- Link your bank account to your brokerage.

- Set $50–100 to go into your index fund each month.

- Let it grow without worrying about timing the market.

Tip: This strategy is called dollar-cost averaging. It means you buy more shares when prices are low and fewer when prices are high, lowering your average cost over time.

Track and Adjust Occasionally

Once you start, don’t panic if prices go up and down.

- Check your investments every 6–12 months.

- If your financial situation changes, you can adjust your monthly amount.

- Stay patient : index fund investing works best for long-term growth.

Diversify as You Grow

Start with one broad fund. Once your portfolio reaches around $10,000, consider adding:

- International index funds (20–30% of portfolio)

- Bond index funds (10–20% for stability as you age)

This keeps your investments balanced and lowers risk.

Benefits of Starting Small

Even with $50–100 per month, you get:

- Exposure to hundreds of companies at once

- Low risk compared to picking single stocks

- A habit of saving and investing for the future

- Growth over time thanks to compounding

Understanding Returns

Different index funds move differently. For example, the S&P 500 may rise 20% in a year, while a sector fund could drop. This is normal. The key is to focus on long-term growth rather than short-term ups and downs.

Key Takeaways

- Starting small : $50–100 per month is enough.

- Use low-fee index funds to spread your risk.

- Automate your investments to stay consistent.

- Be patient and think long-term.

Starting early, even with a little money, gives your investments time to grow and can set you up for a financially strong future.

Further Reading:

- Investopedia: Index Fund Basics

- Vanguard: Getting Started Guide

- SEC: Beginner’s Guide to Asset Allocation

Frequently Asked Questions

1. What happens if I miss a month? Will it ruin my investment strategy?

No, missing a month won’t ruin anything. Life happens, unexpected bills, emergencies, or tight months are normal. Your existing investments keep growing even if you skip a deposit. Resume when you can. Consistency matters more than perfection. If you miss two months, don’t try to “catch up” by doubling your next payment unless your budget allows it. Just restart your regular schedule.

2. Should I invest in index funds or pay off debt first?

It depends on your interest rates. If you have high-interest debt (credit cards at 18-25%), pay that off first. The guaranteed “return” from eliminating 20% interest beats potential 7-10% market gains. For low-interest debt like student loans (3-5%), you can split your money between minimum debt payments and index fund investments. This builds wealth while managing debt responsibly.

Quick Rule: Debt above 7% interest → pay off first. Debt below 5% → invest while paying minimums.

3. Can I lose all my money in an index fund?

Technically yes, but it’s extremely unlikely. For the S&P 500 to hit zero, all 500 major U.S. companies would need to fail simultaneously including Apple, Microsoft, Amazon, and hundreds more. That’s never happened in market history. However, your investment value will fluctuate. You might see temporary drops of 20-30% during recessions. This is normal. If you hold long-term (10+ years), history shows markets recover and grow. Short-term volatility ≠ permanent loss.

4. When can I actually withdraw my money? Is it locked in for years?

You can withdraw anytime index funds aren’t locked accounts. However, smart investors avoid early withdrawals for three reasons:

Tax implications: Selling within one year triggers short-term capital gains tax (higher rate). After one year, you pay long-term capital gains (lower rate).

Lost growth: Money withdrawn can’t compound. Pulling out $1,000 today means losing its potential $2,000+ value in 10 years.

Market timing risk: If you withdraw during a market dip, you lock in losses instead of letting them recover.

Best approach: Treat index funds as long-term savings (5+ years minimum). Keep a separate emergency fund for immediate needs.

5. What’s the difference between ETFs and mutual index funds? Which should I choose?

Both track the same indexes, but they trade differently:

Mutual Index Funds: You buy directly from the fund company (Vanguard, Fidelity). Trades happen once daily after markets close. Often require minimum investments ($1,000-$3,000), though some have $0 minimums. Perfect for automatic monthly investing.

ETFs (Exchange-Traded Funds): Trade like stocks throughout the day on exchanges. No minimum investment but even one share. Sometimes have commission fees depending on your broker.

For $50-100 monthly investors: Mutual index funds work better. Why? Free automatic investments, no trading commissions, and fractional shares built-in. ETFs make more sense for lump-sum investing or traders who want intraday pricing.

6. How do taxes work on index fund gains? Do I owe taxes every year?

Here’s what beginners need to know:

- Capital gains: If you sell your fund for a profit, short-term gains (held ≤ 1 year) are taxed like regular income, while long-term gains (held > 1 year) get lower tax rates.

- Dividends: Any dividends your fund pays are taxable in the year you receive them, even if you automatically reinvest them.

- Tax efficiency: Index funds usually generate fewer taxable events than actively managed funds, making them beginner-friendly.

- Retirement accounts: Using IRAs or 401(k)s lets your money grow tax-deferred (traditional IRA/401(k)) or tax-free (Roth IRA), dramatically boosting long-term growth.

Tip: With $50–100 monthly, a Roth IRA is often the simplest and most effective choice for long-term investing.

7. Should I pick one index fund or spread money across multiple funds?

Starting out with $50-100 monthly? Stick to one broad index fund like a total market fund. Here’s why:

- It already contains 3,000-4,000+ stocks instant diversification

- Multiple small positions increase complexity without adding much benefit

- Lower fees (you’re not paying expense ratios on multiple funds)

When to diversify: Once you reach $10,000+ invested, consider adding:

- International index fund (20-30% of portfolio)

- Bond index fund (10-20% for stability as you age)

The rule: Keep it simple until you have enough assets to meaningfully diversify.

Build a Balanced Portfolio

Follow the Rule of 110: subtract your age from 110 to see how much of your portfolio should be in stocks vs. bonds.

Combine small-cap, large-cap, and international funds for diversification. Limit trend-focused funds (AI, crypto, etc.) until your portfolio grows.

8. How do I know if my index fund is performing well?

Don’t compare month-to-month, that’s too short-term. Instead, check these benchmarks annually:

Performance vs. benchmark: Your S&P 500 fund should closely match S&P 500 index returns (within 0.1-0.2%). If it underperforms significantly, check the expense ratio.

Expense ratio: Should be under 0.20%, ideally under 0.10%. Anything above 0.50% is too high for an index fund.

Tracking error: The difference between your fund and its target index. Lower is better.

Reality check: If the S&P 500 is down 15% and your fund is down 15%, that’s good performance, it’s accurately tracking the index. You’re not trying to beat the market; you’re trying to match it at the lowest cost.

Disclaimer: Investing involves risks, including the potential loss of principal. Past performance of any investment, including index funds, does not guarantee future results. This content is for educational purposes only and does not constitute financial, investment, or tax advice. Always consult a licensed financial advisor before making investment decisions.

Post Disclaimer

The information provided on Financepdia.com is for educational and informational purposes only and should not be considered financial, investment, or trading advice. Cryptocurrency and financial markets are highly volatile and involve significant risk. Readers should conduct their own research (DYOR) and consult with a qualified financial advisor before making any investment decisions. Financepdia.com and its authors are not responsible for any financial losses resulting from actions taken based on the information provided on this website.